Market Overview

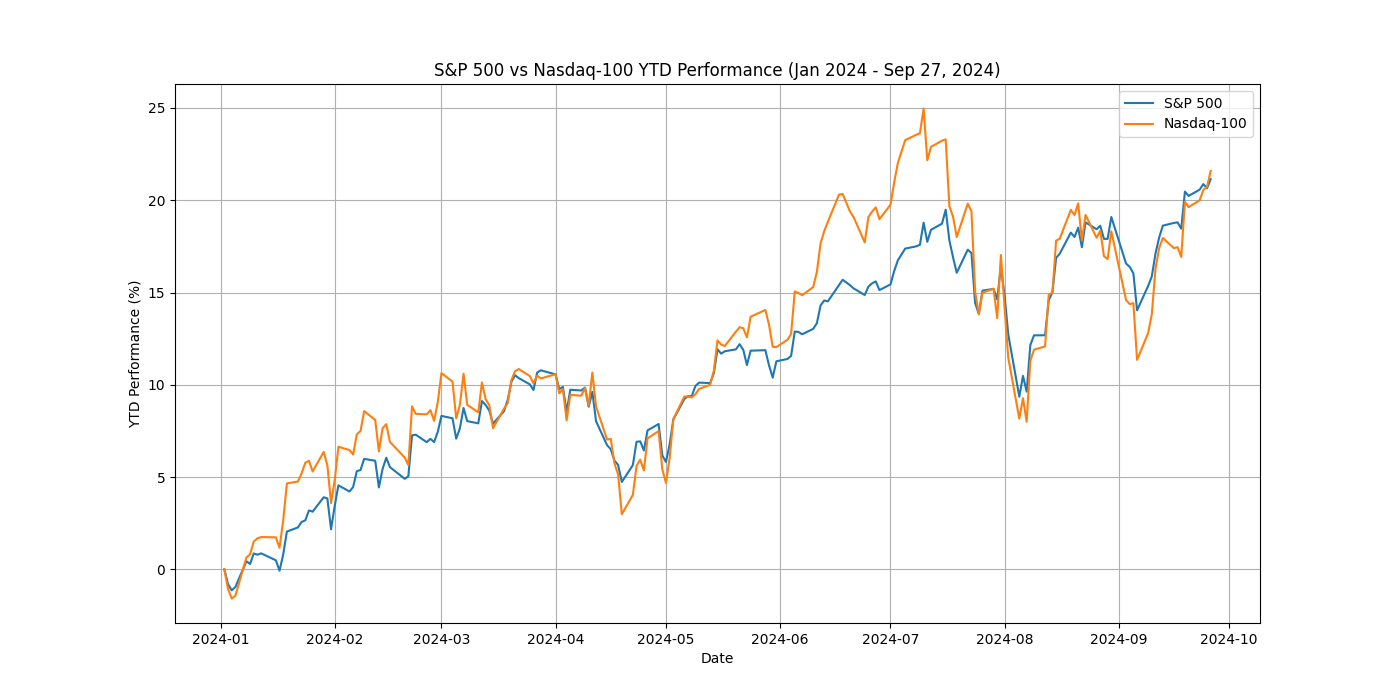

The financial markets experienced significant turbulence during August and September, with the S&P 500 at one point retreating nearly 5% from its all-time high but rallying to less than a percentage point away from its record high and 18% ahead for the year.

Over the past few months, this volatility was primarily driven by mixed economic data, uncertainty about the interest rate trajectory, and a tech sector sell-off, which ended the “Magnificent 7” mega-tech stocks’ phenomenal rally in the first half of 2024.

Recent Market Volatility

August and September have been tumultuous months for investors. The markets initially stumbled in early August, rattled by the Bank of Japan’s unexpected rate hike and the emergence of weak US economic reports, which reintroduced fears of a recession. After rebounding towards the end of August, early September ushered in renewed declines, particularly in the tech sector. Some fears have subsided over the last few days as the market has resumed its climb.

Mixed Economic Indicators in the U.S.

Recent economic indicators have painted a mixed picture of the state of the US economy. While some reports, such as retail sales and industrial production, have shown resilience, others have raised concerns. The labor market, a key focus for the Federal Reserve, has shown signs of cooling, with job openings falling and unemployment claims ticking up. Manufacturing surveys, particularly the NY Fed Manufacturing Survey, have painted a gloomy picture of slowing activity and hiring. These weak economic reports have significantly impacted investor sentiment, contributing to market volatility. They’ve also fueled criticism of the Federal Reserve’s approach, with some arguing that the central bank has been too slow to pivot towards rate cuts, risking a hard landing.

Interest Rate Policy and Its Impact

The Federal Reserve’s commitment to maintaining higher interest rates to combat inflation has been a double-edged sword for the markets. While necessary to tame inflation, which has shown signs of cooling, there are growing concerns about potential over-tightening and its impact on economic growth. The Fed is not expected to reduce rates substantially over the next year unless the US economy deteriorates markedly, which some analysts say could see the central bank reduce rates 10 times by 25 basis points before the end of next year. The Bank of Japan’s decision to raise rates added to global market volatility, prompting an unwinding of the carry trades that have been one of the most popular global trades. Japan’s Nikkei 225 tumbled 12% in early August, prompting Nasdaq to slide 3.4% and the S&P 500 to fall 3%.

Market participants are confident that the Fed is entering a rate-cutting cycle. Futures markets are pricing in 25 to 50 basis point reductions. However, the timing and magnitude of interest rate cuts this year and next are far from certain. Thus, stock markets are likely to remain volatile in the months ahead as further evidence regarding the state of the economy and the resultant interest rate outlook emerges.

Decline in Tech Sector

The tech sector, particularly the so-called “Magnificent Seven” mega-caps (Apple, Microsoft, Alphabet, Amazon, Nvidia, Meta, and Tesla), has underpinned the market’s rally over the past 18 months. These companies have benefited hugely from enthusiasm surrounding artificial intelligence. However, these mega-caps have sold off significantly since early August. Nvidia, for instance, saw its stock price fall 21% from June 20 to September 6 after reaching a record high on June 18, 2024.

Other “Magnificent Seven” stocks have also borne the brunt of the shift in investor sentiment. The dramatic turn in the sector’s fortunes has prompted investors to question whether this shift in expectations is a temporary rotation trade or a fundamental shift in investor views.

At one point, the Nasdaq 100 Index had fallen nearly 9% from its July 10 record, wiping $2.3 trillion off the market value of companies in the benchmark, but it has since gained back some of that ground. Investors’ newfound circumspection has stemmed from valuation concerns and questions regarding the sustainability of the growth rates factored into investors’ outlooks.

Shift to Traditional Stocks

In parallel to the mega-tech sell-off, investors began turning their attention to more traditional stocks, particularly in sectors such as financials, industrials, energy, materials, and healthcare. Several factors drove this rotation:

- Valuation concerns in the tech sector

- The potential for rate cuts, which could benefit traditional sectors

- A search for undervalued opportunities in a market that had become increasingly concentrated

Small-cap stocks were a primary beneficiary of the change in investor appetite, with the Russell 2000 Index of smaller companies climbing 6.6% since the end of June. This divergence was embraced by market analysts who were concerned about the narrow concentration of stocks driving the US stock markets’ rally since last year. A broadening out in the number of sectors contributing to a rising market would be more sustainable.

Economic Data Influencing Federal Reserve Actions

Recent economic data has shown signs of cooling inflation, reinforcing expectations that the Federal Reserve will pivot towards rate cuts. Consumer price inflation declined to 2.5% in August, falling for the fifth month and fueling hopes that this may persuade the Fed to reduce rates by 50 rather than 25 basis points at its September meeting.

However, signs of weakness in some of the labor market data have been a cause for concern for the central bank and private sector analysts. History has shown that unemployment can quickly become a problem.

Unemployment has increased slightly to 4.2% but remains historically low. Weekly jobless claims moved sideways compared to last year, and layoffs are not yet seen as a cause for concern. However, June and July hiring numbers were a worry for financial markets, coming in lower than expected.

Other signs of economic weakness include US factory activity rising less than expected and consumer finances coming under pressure, as reflected in rising credit card defaults.

Outlook for Traditional Stocks

Declining rate cuts are expected to benefit traditional stocks and sectors that have lagged behind the tech-driven rally of the past year. Many of these stocks are trading at more attractive valuations than their tech counterparts, offering potential upside as investors search for value opportunities.

Lower interest rates would particularly benefit rate-sensitive sectors, such as financials and real estate. An improving economy—should the Fed achieve its sought-after “soft landing”—could also drive earnings growth across a broader swath of the market, including traditional stocks.

However, it’s crucial that investors remain alert to the uncertainties that still prevail. US economic policy, global tensions, and the potential for unexpected shocks could disrupt market trends.

Market Dynamics and Investment Strategies

The recent market turbulence and rotation away from tech mega-caps underscore the dynamic nature of financial markets. As we’ve seen, a combination of economic data, interest rate expectations, and sector-specific factors can quickly shift market dynamics.

For investors, the recent market turbulence and rotation away from the “Magnificent Seven” market favorites emphasizes the importance of remaining vigilant and adaptable. While the tech sector’s dominance may be waning, opportunities are emerging in other market segments, and the rotation could create a more balanced and sustainable market rally. As such, investors should remain cautious and look for potential opportunities.

Preparing for Market Changes

Investors must monitor market conditions and be prepared for changes that could arise as the stock market rally evolves. Market leadership could change, with sectors and stocks that have lagged in recent years finding new favor and former market darlings being subject to continued scrutiny. To benefit from these shifts, investors will benefit from maintaining diversified portfolios and ensuring they can capitalize on these emerging opportunities as they arise.

Garnet O. Powell, MBA, CFA is the President & CEO of Allvista Investment Management Inc., a firm with a dedicated team of investment professionals that manage investment portfolios on behalf of individuals, corporations, and trusts to help them reach their investment goals. He has more than 25 years of experience in the financial markets and investing. He is also the Editor-in-Chief of the Canadian Wealth Advisors Network (CWAN) magazine. He can be reached at gpowell@allvista.ca