A Value Investor’s Guide to Five Macro Risks

Global equities held up during April despite persistent inflation, renewed energy price pressure, and a Federal Reserve that looked increasingly divided. Beneath the surface, however, the conditions that sustained the post-pandemic rally, namely cheap capital, narrow leadership, and a market content to price in the best possible outcome, are coming under visible strain.

For value investors, the key question is: What is this business worth under realistic assumptions – and what am I paying for it? When capital was effectively free, that question was easy to sidestep. Growth assumptions could be stretched, and valuations could be justified by narratives rather than numbers. However, that dynamic has changed. The focus has switched to the cost of capital, the durability of a company’s cash flow, and the margin of safety.

These five macro risks are filters through which value is tested, and, for those who prioritize price discipline, opportunities eventually emerge.

- Geopolitics and Energy: Follow the Cash Flows

Oil moved above $100 a barrel during April and briefly surpassed $125 as Strait of Hormuz supply disruptions intensified following continued US-Israeli military operations against Iran. Tehran effectively closed the strait in late February, and while a ceasefire was extended, a naval blockade of Iranian ports remained in place. The effect on energy markets was direct and significant: supply chains for oil, fertilizers, petrochemicals, and aluminium came under simultaneous pressure.

The S&P Global flash US Composite PMI rose to 52.0 in April from 50.3 in March, with manufacturing leading the recovery. But the detail mattered more than the headline: delivery times to factories reached their longest since August 2022, output prices jumped to a near four-year high, and the survey’s measure of prices paid by businesses hit an 11-month high. Companies were building safety stocks rather than meeting genuine demand, a precautionary response that temporarily bolsters activity data while imposing downstream cost pressures.

The value lens

Energy shocks redistribute cash flows across industries, creating both losers and, for patient investors, identifiable opportunities. The likely beneficiaries are integrated oil producers, commodity exporters, energy infrastructure companies, and selected mining groups. These are businesses with asset-backed earnings that benefit directly from higher prices. In commodity-oriented markets and among global energy exporters, resource-heavy companies and diversified industrials with energy exposure stand to benefit.

The likely losers are energy-intensive industrials, consumer-facing businesses exposed to fuel costs, transport and logistics operators, and highly leveraged cyclicals with limited ability to absorb rising input costs. In economies that are net importers of oil, including much of Europe and Asia, consumers and businesses face additional pressure from imported inflation and fuel cost pass-through.

The critical distinction for value investors is between temporary earnings pressure and permanent capital impairment. Volatility of the kind experienced in April can force selling, create sector dislocations, and widen the gap between price and underlying value. That environment favours investors willing to do the fundamental work, identifying businesses where the share price reflects a far worse outcome than the business itself will ultimately deliver.

- Inflation: The Stress Test That Separates Real Businesses From Nominal Ones

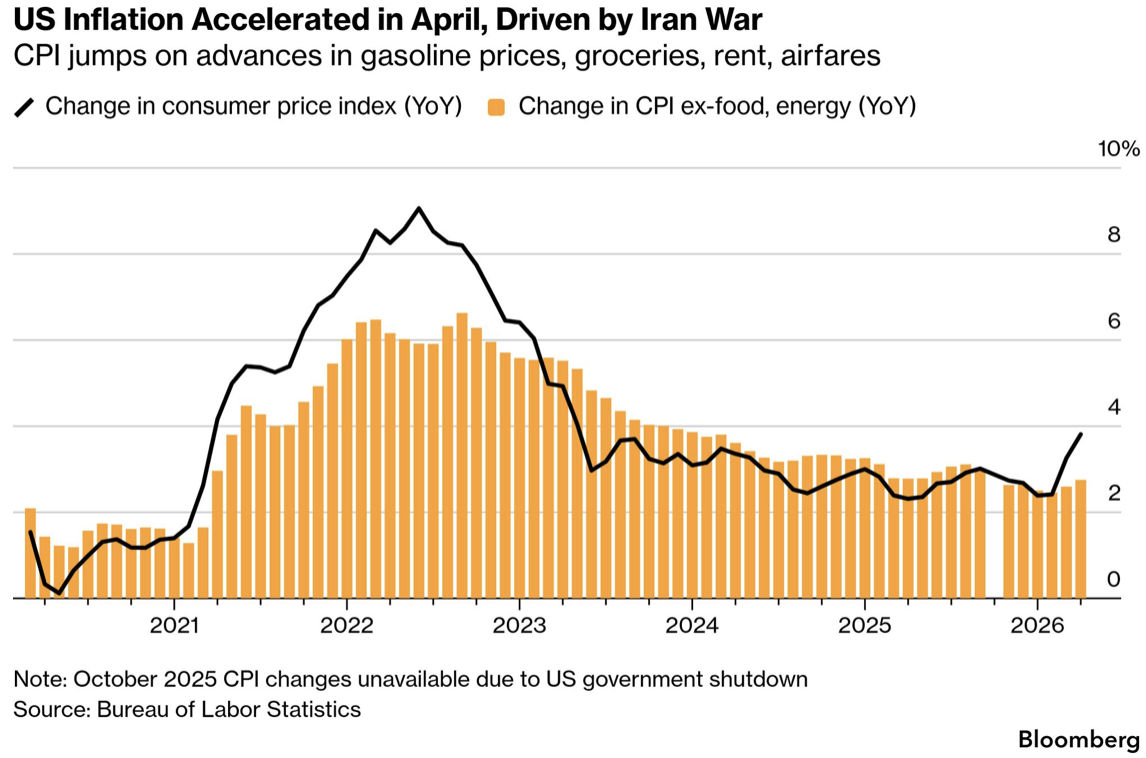

Services inflation remained sticky through April. Wage pressures persisted. And the energy shock layered a fresh commodity impulse on top of an inflation profile that was already firmer than the market had hoped. US inflation data reduced confidence in imminent rate cuts and, combined with supply-chain disruptions, pointed to an acceleration in prices in the months ahead.

The PMI data showed output prices charged by US businesses rose in April at the fastest rate since July 2022. Businesses were paying more for inputs and passing those costs on, or, where they lacked the pricing power to do so, absorbing them into margins.

The value lens

Inflation is one of the most effective filters for assessing business quality. In benign conditions, nominal revenue growth can mask weak unit economics. When costs rise persistently, that mask comes off.

The businesses that perform well through inflation share common characteristics: genuine pricing power rooted in customer necessity or competitive advantage, low capital intensity, asset-light models with recurring revenues, and cost structures that do not expand in step with input prices. Essential service providers and businesses with long-term contracted revenue streams fall into this category.

The businesses that struggle are those that report revenue growth while margins quietly deteriorate. These include: margin-sensitive retailers, labour-intensive operators, commodity-dependent producers with no pricing power, and highly cyclical businesses that relied on the tailwind of falling input costs.

The key insight: nominal growth is not real earnings growth. When assessing any business in an inflationary environment, revenues may be rising, but you need to ascertain whether the business’s economics are genuinely improving or merely inflating in nominal terms.

- Central banks in a policy trap: cost of capital matters again

The Federal Reserve held its policy rate steady at 3.50%–3.75% at its April meeting, as expected. What was not expected was the level of internal division. The vote was the most divided since 1992: eight officials voted to hold, three dissented against the easing bias in the statement, and one voted for a cut. Traders moved to price in no rate cuts for 2026, with a 25% probability of a hike within twelve months.

The statement itself was telling. The Fed dropped the word “somewhat” from its characterization of inflation. It is now simply “elevated”, while acknowledging that the energy shock linked to the Iran conflict is contributing to a “high level of uncertainty.” The incoming Fed chair, Kevin Warsh, will inherit a deeply divided committee in an environment where the case for easing has become considerably harder to make.

The ECB and Bank of England face similar pressures. European yields followed US Treasuries higher, and US 10-year yields moved to 4.30–4.35% during the week of 20–24 April, reflecting inflation repricing rather than growth optimism.

The value lens

Higher discount rates do not affect all businesses equally. Growth assets with long-duration earnings profiles, in other words, businesses priced on the assumption of substantial cash flows far into the future, are disproportionately sensitive to rising rates. When the discount rate rises from 4% to 6%, the present value of cash flows expected 10 years from now falls materially. Valuations that looked defensible at lower rates become difficult to justify.

These conditions favour self-funded companies that generate strong free cash flow and face low refinancing risks. Steer clear of growth stories that depend heavily on capital, companies that are structurally unprofitable and depend on cheap funding, and businesses valued based on a future where interest rates need to drop to post-GFC levels.

A note of caution: markets may still be underestimating the long-term effect of structurally higher real rates on equity valuation multiples. The adjustment may not happen all at once, but the odds point to increasing rates over the next few years.

- Recession Risk: Normalize, Don’t Extrapolate

The economic picture through April was mixed rather than clearly recessionary. Manufacturing activity recovered, partly driven by precautionary stock-building, while the services sector barely stayed in expansion territory. Labour markets remained relatively resilient, though the PMI data noted companies reducing headcount in manufacturing and limiting services employment growth amid uncertain demand and high input prices.

Corporate margins are under pressure from three directions simultaneously: rising input costs, slowing consumer demand, and higher financing costs for leveraged businesses. Earnings downgrade risk has increased, and the combination of “sticky” inflation with softening growth is creating the conditions for a stagflationary episode rather than a clean cyclical slowdown.

The value lens

The most common and most costly mistake in a softening cycle is extrapolating bear-market conditions indefinitely. When markets price in a severe or permanent deterioration in earnings, quality cyclical businesses can trade at substantial discounts to their normalized earnings power, creating the kind of asymmetric opportunity that value investing is designed to exploit.

These can be identified by focusing on mid-cycle or through-the-cycle profitability rather than peak or trough earnings, assessing balance sheet resilience (can this business survive a two-year downturn without dilutive capital raises?), and distinguishing between cyclical impairment, where earnings recover as conditions normalize, and structural impairment, where the competitive position or business model is genuinely and permanently damaged.

Sectors worth examining with this lens include industrials, selected financials, and quality cyclicals in resources, where balance sheets are sound, and valuations already reflect considerable pessimism.

- Valuation and Market Complacency: Where is the Margin of Safety?

The S&P 500 rose roughly 10.5% in its best month since 2020, largely driven by gains in AI-linked technology and communication services in April. Broader equity market participation was capped by oil-driven inflation concerns, and the VIX held between 18 and 19 – elevated but orderly, reflecting caution rather than stress, with investors emphasizing downside protection over upside participation.

The value lens

The biggest risk facing investors is not volatility but overpaying for future expectations that may not materialize. The market’s most expensive segments – those priced for strong growth, falling rates, and near-perfect execution – carry the most downside risk if any of those assumptions prove overly optimistic.

With US equity indices still at historically high valuations relative to long-term averages, in some areas the market is priced for a benign outcome that current macro conditions do not clearly justify. When valuations leave no margin of safety, the market’s tolerance for setbacks tends to become very limited.

Many lower-rated sectors and markets already reflect recession concerns, higher rates, and slower growth in their pricing, potentially creating opportunities for investors willing to look beyond the current narrow list of stocks driving index performance.

Stagflation through a value lens

The April data points suggest the possibility of a stagflationary episode unfolding, with the associated slower growth and persistent inflation threatening to compress consumer spending, corporate margins, and valuation multiples simultaneously.

Historically, value strategies have outperformed growth strategies in this environment. The reason: when inflation erodes the value of promises about future cash flows, investors are forced to assess a business’s fundamentals, including whether it has pricing power, real assets, a strong balance sheet, and a conservative capital allocation to retain and build value. Businesses with excessive leverage or earnings that depend on benign conditions are exposed.

Macro pressures also tend to widen the gap between strong and weak businesses, and patient investors can take advantage of the resulting mispricing.

Discipline in portfolio positioning

The current environment supports value-oriented investors pursuing disciplined portfolio allocation which considers:

- The potential offered by cash-generative businesses with defensive free cash flow profiles, strong balance sheets, reasonable or discounted valuations, dividend sustainability, and asset-backed earnings streams. These offer both downside protection and the ability to compound value through a difficult period.

- Why selectivity is advisable in cyclicals, financials, and resources. Quality within these sectors varies significantly. Focus on cost position, balance-sheet resilience, and management discipline. In a higher-rate, slower-growth environment, the difference between the best and worst operators in a sector widens dramatically.

- Why it is sensible to avoid excessively speculative growth stories, businesses priced for perfection, and companies dependent on refinancing at rates that no longer exist.

For investors with exposure to commodity-oriented markets and global resource equities, the current environment offers specific advantages: direct commodity exposure, currency diversification through global revenue earners, and selected defensive franchises trading at valuations that already reflect a degree of macro pessimism.

Rationality over forecasting outcomes

Macro uncertainty in April 2026 was exceptionally elevated. The Iran conflict, a divided Federal Reserve, sticky inflation, and slowing growth created an uneasy backdrop. Markets held up, but were increasingly dependent on a small number of counters.

For the value investor, none of this is unusual, as uncertainty is an indelible feature of investing, and the focus should be on rationally pricing its impact. Value investors’ edge lies in their willingness to do careful fundamental work, pay a price that reflects realistic rather than overly optimistic assumptions, and maintain the patience to wait for that discipline to pay off.

Garnet O. Powell, MBA, CFA, is the President & CEO of Allvista Investment Management Inc., a firm that manages investment portfolios on behalf of individuals, corporations, and trusts to help them reach their investment goals. He has more than 25 years of experience in the financial markets and investing. He is also the Editor-in-Chief of the Canadian Wealth Advisors Network (CWAN) magazine. He can be reached at gpowell@allvista.ca